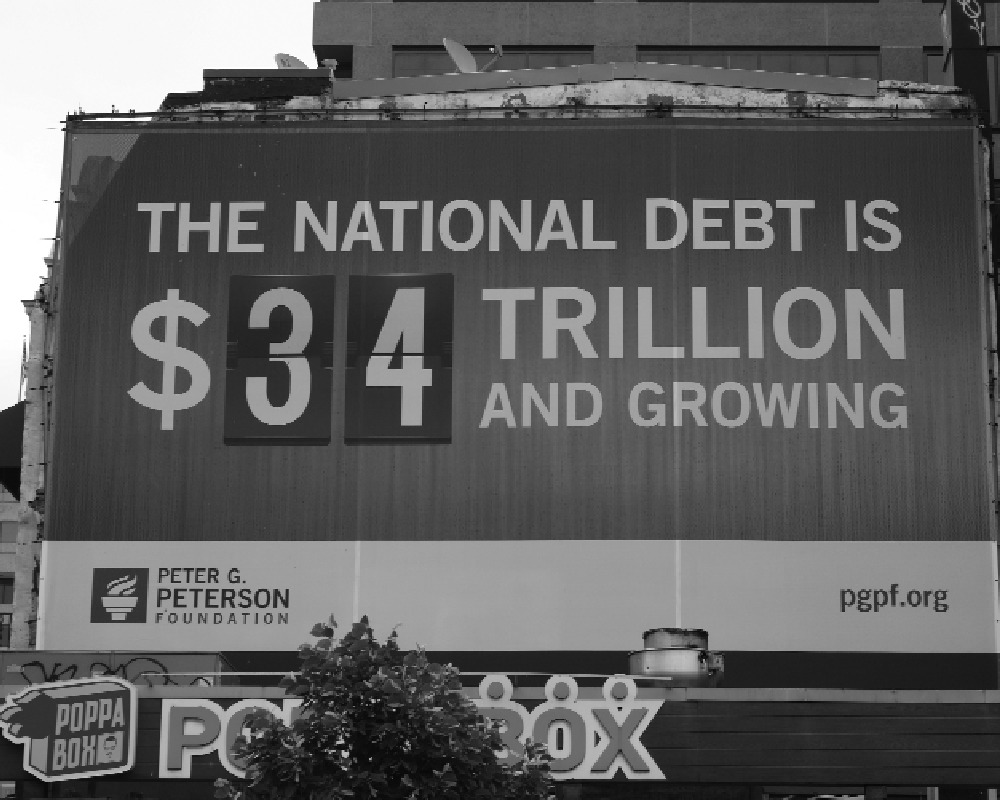

As gold prices gallop northwards, and the rise seems unstoppable, several theories, including the conspiratorial ones, have begun to hog the headlines in the mainstream media, and content on social media. Yesterday, in this column, we referred to the theory that BRICS was behind the unusual demand for gold among the central banks, institutions, and retail investors. Today, we will flesh out a more sinister theory. One of the superpowers is covertly driving gold prices up to resolve and sort out its trickiest and most dangerous economic issue. Of course, the country is NOT China, but America. The main challenge the latter faces is not related to trade or tariff, inflation or growth, or jobs or salaries. It is about debt. Although the photograph with this piece suggests the figure to be $34 trillion, it has since increased further by another two trillion dollars.

But what do gold prices and demand have to do with a nation’s debt? Let us look at the facts, both related to gold and debt. At present, the US holds the highest gold reserves among nations, with more than 8,000 tonnes. Most of it is stored in secure depositories such as Fort Knox, Federal Reserve Bank of New York, and West Point (a military base). This explains the Hollywood movies with plots to steal the gold from Fort Knox. The substantial reserves of the yellow metal are an important reason for the global dominance of the dollar, and nations’ trust in the currency. Of late, this supremacy and trust have dented quite a bit. At September 2025 prices, the market value of the gold with the US is a trillion dollars. In its books, however, it is valued at the 1973 prices, or a mere 11 billion.

America’s national debt, as we mentioned earlier, is $36 trillion, and growing by each minute. The debt-to-GDP ratio is 125 per cent, which implies that what it owes is higher than what the economy generates every year. Obviously, the negatives are rooted in ballooning annual fiscal deficits which, in recent times, were accelerated by bailouts, defence spending, and pandemic-related stimulus, which ran into trillions of dollars. The annual cost of servicing this debt, which was over $700 billion in 2023, or 14 per cent of the total federal spending, is expected to zoom to $1.4 trillion by 2033. Clearly, it is an unsustainable and precarious financial situation. Something will need to give, and soon. The US economy cannot absorb future debt-interest payment shocks. Trade and tariffs, and jobs and growth can reverse within months or years. Loans and interest grow forever, unless one pays them in time.

Now, for the kicker-sucker punch. If the US re-values its gold reserves, and marks it to market, or current prices, the book value will jump to more than a trillion dollars, or “an instant windfall” for the economy. This will happen without the fresh sales of new debt (Treasury bills) or asset classes. The nation’s balance sheet improves in a jiffy. The gold shine will work magic on its financials and debt. According to a media report, “Some financial commentators have called it a ‘nuclear option’ to boost the US sovereign credit in the face of historic deficits.” The adjustment, says an analyst, will “wipe out a trillion dollars in debt.” So, the rise and rise in gold prices suits the US. In the recent past, gold buying by the US institutions has gone up by 1,300 tonnes, although the Federal Reserve has stayed away.

Of course, it is not a win-win game. It is not even a zero-sum one. In fact, the gold-debt play is like snakes and ladders. There are enough reasons to predict a win. There are equal factors to signal a loss. Some experts feel that if the US re-values the gold reserves, there will be an adverse impact on inflation, which may go up, and the dollar, which may tumble against other currencies. The message to the world will be that America no longer has the gold cushion and, hence, the future of the dollar will depend on the economy. If the present trends continue, and other nations and alliances prepare to attack and subsume the dollar, things may not be rosy. The counter is that the “dollar dynamics are different; if gold gets stronger, the dollar will remain strong.” The future of the dollar is pegged to gold prices.

Ironic though it may sound, some commentators imply that the present American debt is linked to gold. Indeed, they see the origins in that day when the former president, Richard Nixon, delinked the currency from gold, or suspended the dollar's convertibility into gold. Before 1971, 35 dollars could be exchanged for an ounce of gold. It was no longer true after the president delivered the “Nixon shock.” Now, the dollar became a free-floating currency, as did the currencies of the other nations. The Gold Standard was discarded. According to a book, this led to unfettered government spending, without checks and balances. Instead of slashing spending, or raising taxes, they could do the opposite, lower taxes, and hike spending. Since the dollar was not linked to the gold reserves, the governments merely ran deficits.